7 4: Equivalent Unit Calculations Business LibreTexts

None of the ten units is complete; merely the equivalent amount of work necessary to complete three units is said to have been performed. If the firm frequently has significant swings in per-unit costs, the weighted average method is less appropriate. It holds workers and managers accountable, in part, for cost decisions from prior periods. When each individual product unit is the same, managers are not going to spend time thinking about individual product units—they’re all the same!

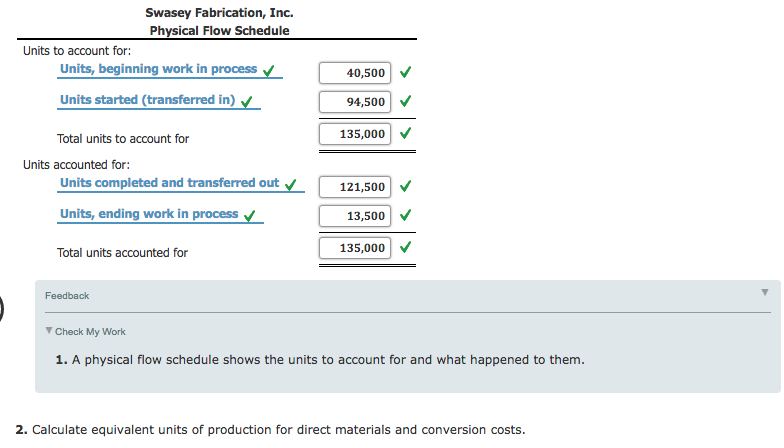

1.2 Complication #1: Units in Ending WIP Inventory

It shows that 650,000 units were transferred on to the Skim/Alloy Department, leaving 250,000 tons still in process. When goods are produced in a continuous process, how are costs to be allocated between work in process and finished goods? Accountants have devised the concept of an equivalent unit, a physical unit expressed in terms of a finished unit. When Department A is done with some product units and passes those units onward to Department B, then we credit the WIP-A account for the cost of those units and debit the WIP-B account for the cost of those units. Let’s update our overhead allocation equation to incorporate our first complication of equivalent units. For example, during the month of July, Rock City Percussion purchased raw material inventory of $25,000 for the shaping department.

Why You Can Trust Finance Strategists

Essentially saying, that process 1 completed 850 units to completion of process 1 in this period. Add that $860 to whatever we figured was the conversion cost of Units Started and Completed and we have the total conversion costs of units completed and transferred out. However this unit probably may already have most if not all of its direct materials, i.e. ~100% complete with respect to direct materials. 100% of the wood that needs to be painted, 100% of the clay that needs to be baked, or 100% of the metal that needs to be polished is already on the assembly line.

Process Costing – FIFO Method

(1) Get a pot of water out (equipment and water costs are likely overhead). Take self-paced courses to master the fundamentals of finance and connect with like-minded individuals. Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs.

Estimating the Percentage of Completion

The overhead cost per unit number has now transformed into an overhead cost per equivalent unit number. To reiterate, this allows the overhead cost we allocated to ending WIP units to be scaled by those ending WIP units’ percent completion. In this method, both the beginning and ending inventory is converted into equivalent units, so there is a bit more work to do. For those units that were in the what is form 1095 beginning inventory, we need to figure out how much work was DONE on them in this period to get them to the point of being transferred to the next process. For those items in the ending inventory, it is the same as the weighted-average method, where we need to calculate how much work has been done to them already. Our equivalent units of production for the period is 1,200 units (700 + 500).

However, the units in ending work in process require more thoughtful consideration. What this example shows is that although there are 300 physical units of product in work in process, as they are only 40% complete it is equivalent to having 120 units of finished, fully completed product. Equivalent units are calculated by multiply the number of physical units in work in process by the estimated percentage of completion of the units. The extra step is to directly add beginning WIP cost to the units completed (see cells D6, D13, and D20 in the above figure). We’ll use these total equivalent units numbers in the denominator to calculate cost rates.

First, FIFO only applies this period‘s rate to work done this period. So, the beginning WIP equivalent units are subtracted away in order to arrive at “Equivalent units completed with this period’s work” (see cells E4, E11, and E18). That removes the portion of beginning WIP units that were completed last period. We already covered how the weighted average and FIFO methods define the denominators differently.

- All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

- No units were lost to spoilage, which consists of any units that are not fit for sale due to breakage or other imperfections.

- First, product costs (meaning direct materials, direct labor, and overhead).

- As you examine the diagram, think of the amountof water in the glasses as costs that the company has alreadyincurred.

Finally, the equivalent units of production calculated via the previous three steps should be aggregated to ascertain the total output in terms of equivalent units or equivalent production. Under FIFO, remember to bring over the costs of beginning work in process first, then multiply the individual equivalent units calculated in step 2 (not the total equivalent units) by the cost per equivalent unit from step 3. To illustrate more completely the operation of the FIFO process cost method, we use an example of the month of June production costs for a company’s Department B. Department B adds materials only at the beginning of processing.

For example, the closing stock of 200 units in a process, with 60% complete in respect of materials, wages, and overheads, is equivalent to 120 units (i.e., 200 x 60%), which are 100% complete. Let us use the same example as in the article on process costing under weighted average method. Under FIFO, we are only interested in the current period costs which is June for this example. Ending work in process inventory was 1/3 complete as to conversion costs. For example, ten units in process that are 30% complete equate to three equivalent units of output.

This leads to $1,006,881.19 credited to this department’s WIP account. That amount is either debited to the next department’s WIP account or to finished goods (if this is the last department in the production chain). Let’s say your department cooks dumplings (a prior department prepared the dumplings; your job is just to cook them). While this is indeed the basic structure of process costing, there are three big complications. This involves deducting the closing work-in-progress from the amount introduced in the process during the current period. The first stage in Navarro’s production process is the Melting Department.